Macro Thoughts On Carbon And A New Conversation on Value

Macro Thoughts On Carbon And A New Conversation on Value

Note: None of the following is indicative of the product design of Open Forest Protocol. It is speculative in nature on the theory surrounding carbon credits and its implications for our theories of value and money specifically. This is not financial advise.

As we build Open Forest there has been a lot of public discussion surrounding carbon credits. VC’s, investors, banks, and so on are all scoping this new emerging landscape. Some have said that credits are no better than virtue signaling and will fail to materialize into a coherent market. Others, believe that we will see 20 - 30x uptick in demand for carbon in the next decade due to a slowed transition, and government (top-down) as well as consumer (bottom-up) pressure to offset corporate carbon footprints.

I want to put forward a nuanced thesis on carbon, and then talk about where I see it going, and how Open Forest is going to be ground zero for this ‘evolution’ in how we understand and manage value:

Carbon credits are the start of a conversation on the value of nature and as an extension, the nature of value. This is a young conversation that inevitably leads to the understanding that nature cannot be valued only from the benign interests of corporations. An asset is purchased. But a value is transacted. Inevitably this conversation on the nature of value and the value of nature leads to the basis for a new monetary system grounded in nature whereby nature is the basis of finance, and not the object of financialization. Basically, carbon is the clown out of the box. Its over. We have officially accepted some form of natural value and now it only grows more. And here is the final hook: carbon is the start of a new conversation on the nature of value and crypto is the beginning of the internet of value.

There is a lot bundled up inside of this thesis, so below, I would like to unravel it piece by piece for the full impact of it to show itself. Let’s start with the beginning:

Carbon credits are the start of a conversation on the value of nature and as an extension, the nature of value.

For the first time ever, we are creating value from nature. From a value-flow perspective, this means that an ‘expert’ measures carbon stocks in a forest, and is able to issue a unit of value ‘a credit’ for the estimated measurement. This credit is then sold for money, with the purchaser either re-selling it on a market, or ‘retiring’ it from the market as a mechanism for offsetting a carbon footprint.

The reason it is the start of a conversation, is because there are a lot of loose ends and unclear reasons for doing something in relation to the issuance of value as it relates to nature.

What are the parameters from which this value can be issued?

Why is soil carbon not considered for some (forest credits), while it is considered for others (Mangroves for example).

What designates ‘avoided deforestation’ as having been under probable threat?

Does that probable threat of deforestation have to have been present, or should larger trends be taken into account?

What qualifies as ‘additional’ and who decides that? Who decides who decides?

This is a young conversation that inevitably leads to the understanding that nature cannot be valued only from the benign interests of corporations. An asset is purchased. But a value is transacted.

How do we see this ending - 100, 200, 300 years from now? Are carbon credits going to be a temporary blip in history - a hold-over of sorts - while companies ‘transition’ to a more sustainable energy program?

There are a couple of fundamental problems with this, if this is the thesis - largely because the transition to ‘clean energy’ has an elephant in the room, as well as an not-accepted consequence. The elephant in the room is that the transition is going to take much longer than we might expect (see below), and the not-accepted consequence is that a draw-down in CO2 emissions, is not directly correlated with a drawdown in natural extraction, species extinction, and destruction of nature (all things we very much indirectly depend upon). That is to say, a company might be ‘clean’ in how it generates or consumes energy - but still might work in a detrimental way towards our environment. New resorts replacing mangrove forests, deforestation of land for farming, pollution of water from mining or over-extraction of water from natural reservoirs are a couple of examples that come to mind.

So back again to the key question: How does this end? An asset is purchased. Do we realistically see this market lasting the duration of the entire ‘transition’? What does this mean for nature? Are we content, with hooking the entire future preservation of nature on the premise that nature is an asset, that is to be bought or financialized by those looking to ‘offset’ their CO2 emitting behavior?

Inevitably this conversation on the nature of value and the value of nature leads to the basis for a new monetary system grounded in nature whereby nature is the basis of finance, and not the object of financialization.

Once we accept that nature has value. And we accept that assets are purchased, while value is transacted, we move towards a more mature conversation about how we would like to relate to nature - specifically with our monetary tools of value. Nature should not be an object of financialization as much as it is the basis of finance. And I mean this latter statement quite seriously. The forest shelters the water, and water is the basis of life. Get rid of the forest, wait for the water to go, and then life - and all of the many things inside of it inevitably collapse - and we are living in a synthetic reality on mars (or maybe Venus is more analogous).

Basically, carbon is the clown out of the box. Its over. We have officially accepted some form of natural value and now it only grows more.

We HAVE already accepted carbon credits as abstracted units of real monetary value. The conversation has kicked off. Every corporation with a reduction ‘drawdown’ pledge, or every corporation that has bought credits to offset has accepted this new asset of value. And if Nature has value, then why are we only valuing the carbon? What about the biodiversity? What about the animal species? The fresh water? And from there, why as an asset that is purchased - and not as a fundamental value itself?

And here is the final hook: carbon is the start of a new conversation on the nature of value and crypto is the beginning of the internet of value.

Enter Crypto:

Crypto holds the promise of fast-tracking how we are able to expand the carbon asset class, and also transition towards backing our value - with nature. Composability between dApps, tokenization of inputs or data, and communication between smart contracts is well-positioned to rapidly expedite our conversation on the value of nature. And since the cat is out of the bag, another explosion of experiments is most likely to follow in testing out what scales, and what works best.

More importantly, Crypto is a voice from outside of the existing system, where new decisions can be made, and the conversation can continue outside of traditional structures of power over the value of nature. Should the parameters for ‘additionality’ change as we continue to lose millions of hectares of forest each year? Should we try out new or more long-term, macro-focused incentive schemes to try to fix our relationship with nature? What does everyone else not included in the conversation up until this point, actually value?

We are moving - very quickly - to a shift in the conversation. Binary relationships between nature-projects and consultant-verifiers, are in for a very interesting reckoning when systematic relationships between network-protocols and nature-projects become possible. And it will not only be about price. It is also about access, protection from shocks (a system absorbs shocks much better than a binary relationship), integration with other forms of value, and community participation.

So in the final analysis of this thesis, Crypto is the current that will expedite a new conversation on the value of nature - and as a result the nature of value itself. I believe we are only at the beginning. And we are preparing to disrupt and move this conversation along quite radically using Open Forest.

Post Script. Future Prospects for the Demand of Carbon:

This is more than anything a landscape orientation on where we stand on a ‘green’ transition, and how that might impact our understanding of ‘carbon credits’. If you follow some of the recent talks by Peter Zeihan you will be familiar with his thesis on a green transition (see timestamps in description). Below I want to go through some of the graphics he shows, in what I believe comprise a pretty thorough examination of the bottlenecks to come. His analysis, ends, where we then have to take the implications of that for carbon and its price going forward:

This image shows our total energy use of all types of fuels. The point is, we have a ways to go as of 2020, to moving towards a ‘clean energy economy’.

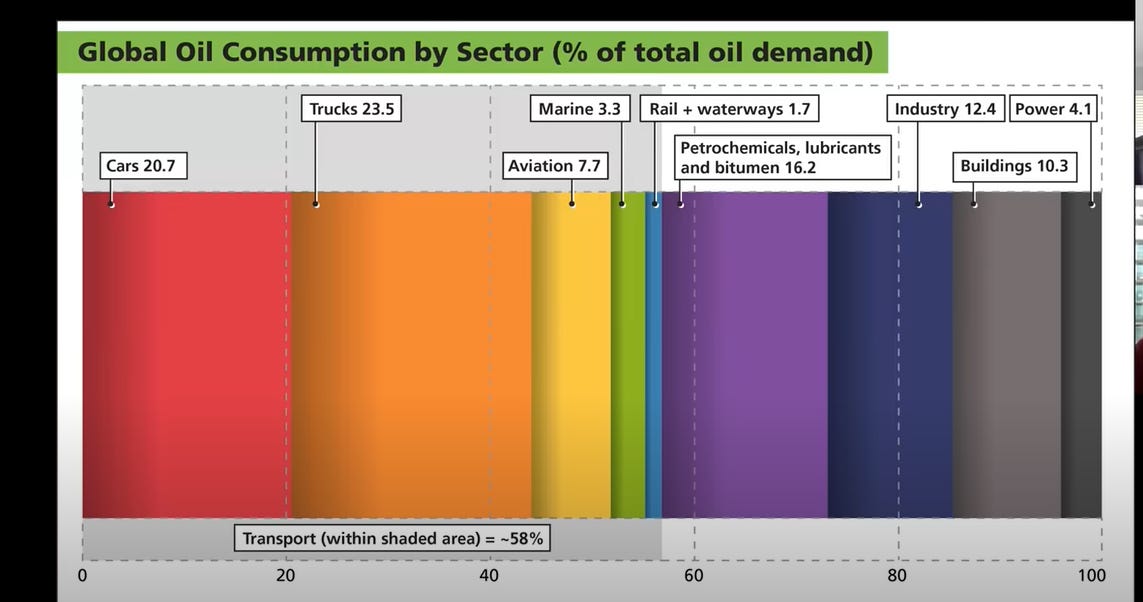

This graphic shows that 58% of global oil consumption (so 58% from the 38% above) is due to transportation. This would argue strongly in favor for the need for electric vehicles.

This shows what materials are used to build those electric vehicles. But also note the need for copper and nickel for things like nuclear power, Solar PV, Coal, and Wind. There is a competition among power-generating technologies, for copper specifically, with nickel still being important and cobalt not insignificant.

And the green arrows indicate how many of these materials will have to be accessed through entirely new supply chains, assuming an extended conflict in Ukraine. Largely due to the number of materials that are exported by either Russia or Ukraine.

To quote Peter in his talk:

“The supply chains for oil are terrible. But if we are serious about moving off from oil, we have to replace that one messy supply chain with 11 more. And then we have to regularly deal with Mexico and Canada, and Venezuela, and Colombia, and Peru, and Chile, and Argentina, and Australia, Indonesia, and Malaysia, and Egypt, and Congo and DRC, and India and Kazakhstan and China, and Russia. We can have a world where the USA uses Oil and the USA is okay without global supply chains. We have got the supplies.

We cannot do the green transition without a life system. There is no way that green tech in their current form, or electric vehicles in their current form can be part of any climate solution. Cause we are not going to have the materials to build the stuff in the first place. Now this is less true in the Western hemisphere than the East. If you add in Australia and SE Asia, we can make a lot of progress, but we can only get about 80% there. And that is not enough to make things work.”

In short, if you believe Peter - who, granted, is not always right on everything - then we are looking at a delayed - at best - energy transition. As I see it, it is a materials science, and a supply chain problem before it is even a business problem. No amount of interest or desire will un-fuck or expedite the creation of new supply chains, barring a major material science breakthrough. This is by no means comprehensive, but it is suggestive.

With this in mind, we can then look at some charts about Carbon and get a sense about what people are thinking:

Tldr, the market for carbon is young, to the extent that MRV has not been prioritized, which by inference suggests that little has been done on the nature based front to protect or create new natural carbon sinks.

Venture Capital has been betting the house on EV and Transportation, which will most likely feel the supply-chain shock as indicated above. Meanwhile, the major discrepancy is once more with nature: Ecosystem Restoration potential vs money into the problem. It’s a young market, once again.

Reading the last two trends into this third picture, we can generally see this lack of financing and investment is actually exacerbating the problem with major losses reported across almost all forest regions in the last 10 years. Not only is natural carbon not prioritized, despite its potential, but it is also losing carbon year over year.

Zooming out, in the Macro of CO2 emissions, lots of talk, little action, less impact - curve go up.

From the EY Net Zero Center Report. Four scenarios. Estimates putting carbon HIGH. Sounds almost too high, but has a delayed transition been priced in, alongside a supply squeeze? Also note, the ‘nature-enabled’ scenario, and the high cost expected from such nature credits.

2035 (13 years) is the amount of time predicted for carbon credit growth until it plateaus. Note the key qualification: “The analysis assumes that markets will evolve towards more efficient supply chain arrangements in order to achieve this dramatic increase in scale.” Internal abatement is listed as an uncertainty. And in total? At least a 20 fold increase that could go as high as 30 to 40 fold.

Okay final graphic. The Sylvera Report on change in available inventory. Note: It’s Negative, and potentially, deeply negative pending the demand scenario.

My final thought: We are stalling our green transition and not invested sufficiently in nature-based solutions (despite their potential) and looking at negative inventory for expected skyrocketing demand of Carbon credits (up to 30 - 40 fold) in next 13 years. I think there is no better time to start, and move this conversation along for the future that is before us.

Not financial advise.

This is pure gold, or should I say, Carbon

but friend, why would an a productive agent have any motivation to join a carbon market? if such agents don't join, how does anything change?